Fluctuations in the market are an inherent aspect of investing, and 2025 has been no exception. While downturns like the tariff-related volatility in April may create discomfort, they can present great buying opportunities. Conversely, when markets rebound and hit new all-time highs, some investors may feel concerned despite solid fundamentals. In either situation, maintaining portfolios designed to handle various market conditions while keeping long-term objectives in focus is crucial.

As we enter the final quarter of 2025, investors are met with mixed signals. In the third quarter, the S&P 500 set record highs bolstered by strong corporate profits and artificial intelligence excitement. However, employment conditions have weakened significantly since early summer, sparking questions about economic strength and consumer financial stability. Furthermore, GDP growth has remained solid and inflation has been relatively contained.

Current market conditions highlight the value of disciplined, long-term investment strategies and financial planning. Instead of responding to news cycles and economic data, maintaining well-diversified portfolios built to handle market transitions is essential. This demands understanding the historical trends that will influence markets going forward.

Third quarter performance highlights

Major indices delivered strong returns during the third quarter, with the S&P 500, Nasdaq, and Dow Jones Industrial Average increasing 7.8%, 11.2%, and 5.2%, respectively. All three reached new highs in September. Year-to-date, these indices have gained 13.7%, 17.3%, and 9.1% respectively. Fixed income also performed well as the Bloomberg U.S. Aggregate Bond Index gained 2.0% in the third quarter and is up 6.1% this year. The 10-year Treasury yield ended the quarter at 4.15%.

International stocks continue their strong performance this year with developed markets (MSCI EAFE) increasing 4.2% in the third quarter while emerging markets (MSCI EM) jumped 10.1%.

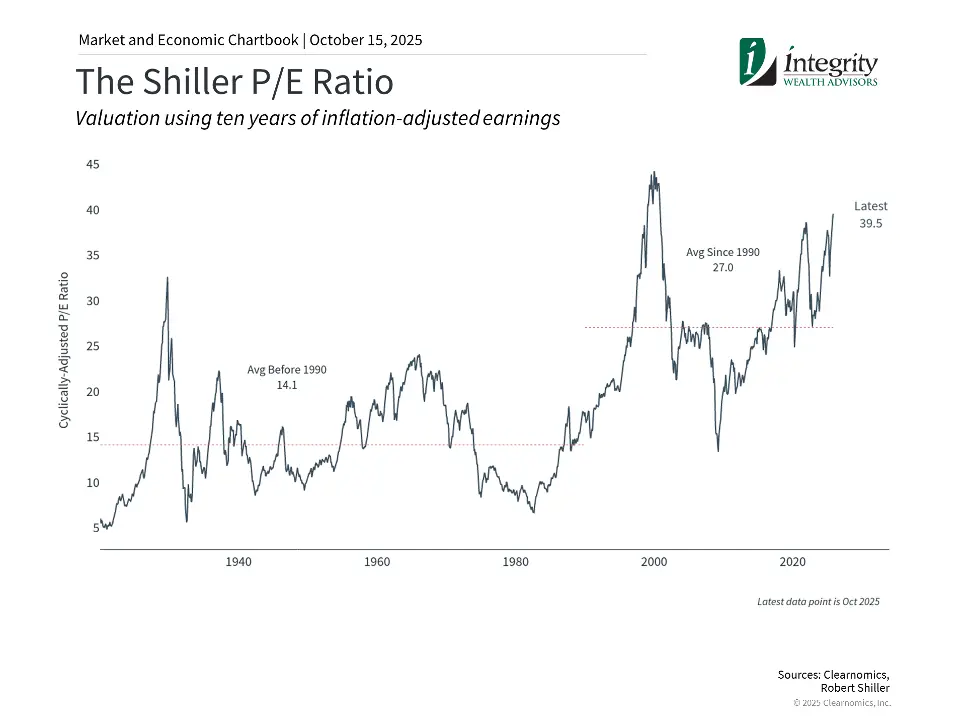

Market valuations approaching historical extremes

Long-term investors use overall market valuation levels to highlight what they receive in exchange for market prices in terms of earnings, cash flow, and other fundamental metrics. While elevated valuations indicate investor optimism, they also suggest expectations may be excessive in certain market segments.

The chart above illustrates this through the Shiller price-to-earnings ratio for the S&P 500. The current reading of 38x exceeds the 35-year average of 27x. This metric offers longer-term perspective by utilizing ten years of inflation-adjusted earnings history. These valuation levels reflect the strong and somewhat surprising recovery over recent quarters.

The S&P 500 has climbed 34% since April 8, producing double-digit gains year-to-date. Technology stocks have led both the recent advance and previous decline, with the Magnificent 7 rising 61% from the bottom. Artificial intelligence investments continue to make headlines due to volatility, yet overall market performance has benefited from increased business spending in this area in particular.

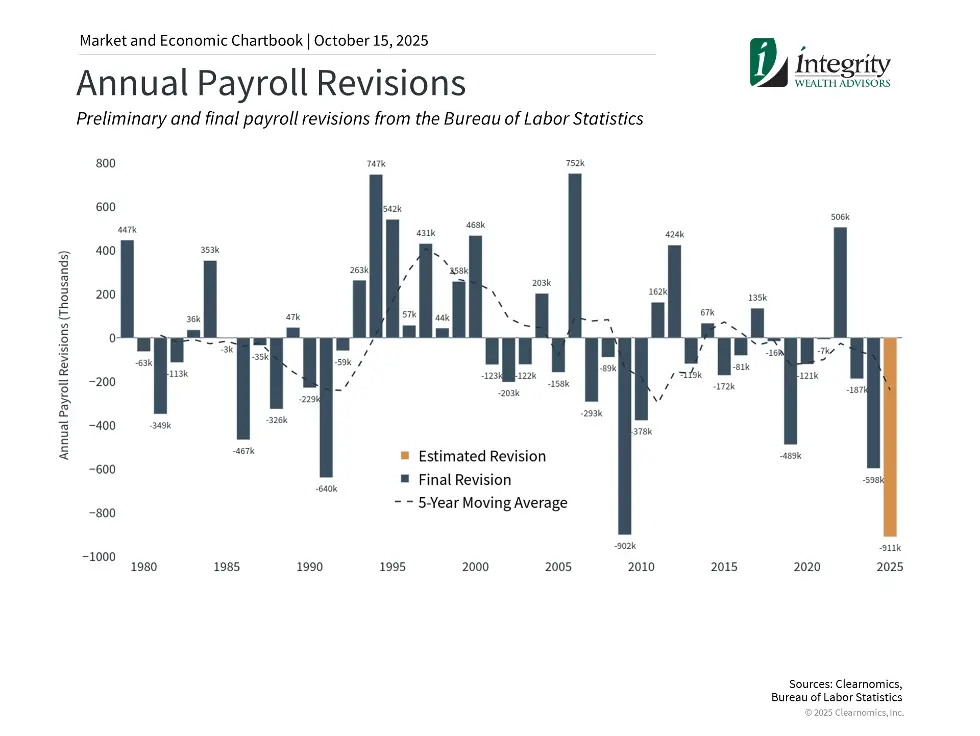

Employment weakness prompts Fed rate cuts

The Federal Reserve’s September 2025 rate cut of 0.25% was the first reduction of the year. This decision attempts to balance inflation remaining above the 2% target with weakening labor market conditions. Public markets expected this rate cut and are also anticipating one to two more before year end. Recent cuts represent a return to normal Fed policy following the rapid 2022 rate hike cycle, explaining why the Fed is easing despite economic expansion and record market levels.

Job market deterioration has arguably been the primary factor influencing the Fed’s decision. Though the 4.3% unemployment rate remains historically low, job creation has slowed dramatically. August added only 22,000 new payrolls, well below the earlier 123,000 monthly average. More significantly, Bureau of Labor Statistics revisions suggest 911,000 fewer jobs were created over twelve months through March than initially reported—potentially the largest revision in history, indicating weaker labor market conditions than previously understood.

Policy uncertainty and volatility have calmed

Earlier this year, investors experienced significant volatility driven by tariff headlines and tax policy uncertainty. The second and third quarters have benefited from the cooling of economic policy apprehension. However, calm periods can shift rapidly. Recent years have experienced numerous volatility episodes from inflation, trade disputes, policy changes, recession concerns, and geopolitical conflicts. Moving into the fourth quarter, events like government shutdowns could create short-term market disruptions despite limited long-term effects.

While unpredictability creates discomfort, it also drives long-term portfolio results. Recent years have demonstrated the gap between investor fears and actual market performance. Successful long-term investors recognize uncertainty as a market characteristic that creates positioning opportunities for future years.

The final quarter of the year is filled with hustle and bustle. Integrity would like to wish all our clients, family and friends a joyous holiday season. May you enjoy time of gratitude, togetherness, generosity and peace.