Dear Valued Clients and Friends of Integrity,

We made it! What a year filled with both turmoil and triumph. As we think back on 2024, let’s start with a review of an abbreviated list of what we experienced during the year – children deaf from birth receiving their hearing for the first time, death of a former president, Paris Olympics, major bridge collapse, multiple hurricanes, total solar eclipse, wars overseas, SpaceX rocket returning to its launch tower, Presidential debates/withdrawals/assassination attempts/conclusion, a ceasefire in the Middle East, and we can’t forget Snoop Dogg.

Every year seems like “it’s different this time”. For some people impacted by the natural disasters and the other negative events during the year, it actually was different and their lives will be forever changed. Our hearts go out to them. For the rest of us, while the minutiae of 2024 were different than prior years, in the grand scheme of things, is it ever really that different? Despite the volatile world we lived through in 2024, the global equity markets stood strong following an even stronger 2023. As we step into a new year, let’s take this opportunity to reflect on the developments that defined the financials of 2024.

Market Returns

2024 was a robust year for market performance, with major indices delivering compelling gains despite widespread uncertainty:

Global Equities (Stocks)

- The S&P 500 (US Stocks) surged by 25.0%, including dividends. This follows a 2023 return of 26.3%

- The Nasdaq 100 and Dow Jones Industrial Average (US Stocks) posted returns of 25.9% and 15.0%, respectively. The 2023 returns were 55.1% and 16.2%

- International stocks also posted positive returns with emerging markets growing 8.1% and developed markets gaining 4.3%. This follows 2023 returns of 10.3% and 18.9%, respectively

- That makes two consecutive years of excellent returns for the global equity markets

- The 2024 results came in a year marked by concerns (potential storms) around the world about inflation, central bank policy (including our own Federal Reserve), and presidential elections in over 30 countries

Fixed Income (Bonds)

- The US investment-grade bond market ended the year slightly positive with a return of 1.3%, as Federal Reserve rate cuts drove policy rates down by a full percentage point. The 2023 return was 5.5%

- Rates for longer-term bonds remained elevated, with the 10-year Treasury yield closing the year just under 4.6% (3.9% at year-end 2023)

- High yield bonds followed up a 13.4% return in 2023 with another 8.2% of growth in 2024

If You Are Already Invested, Stay Invested

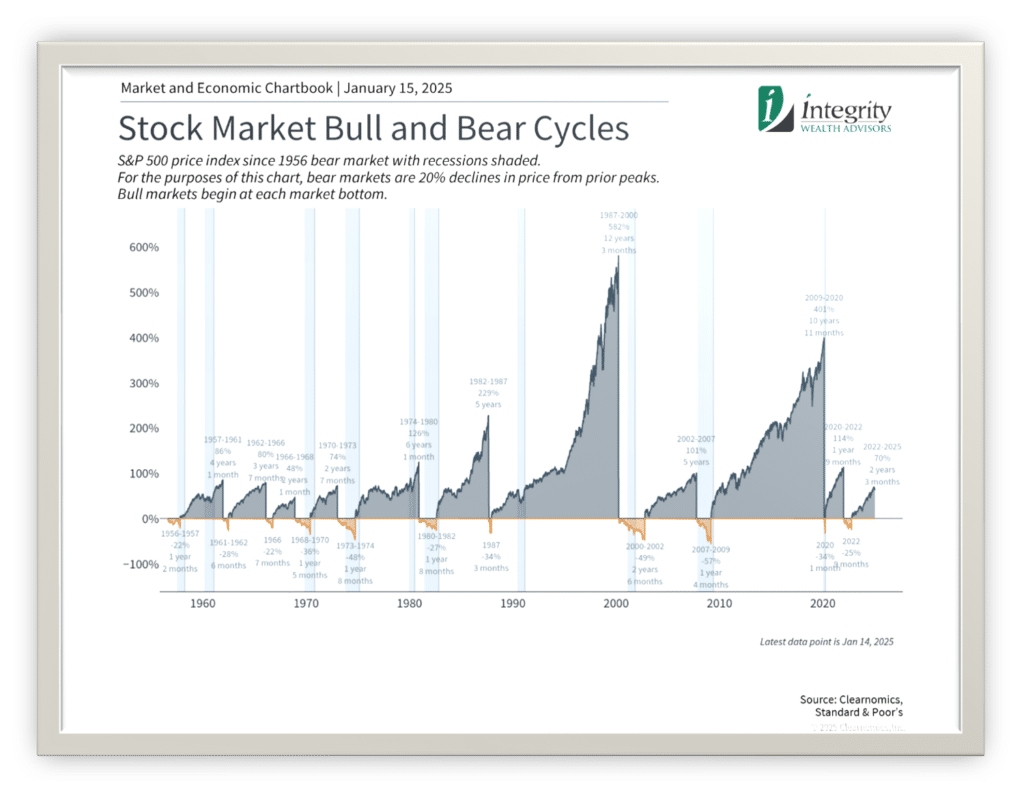

2024 underscored the importance of staying disciplined (i.e. staying invested) during periods of uncertainty. The chart below provides perspective on both bull markets (markets on an extended run upward) and bear markets (markets on an extended run downward). Bear markets (in yellow) are painful, but are generally much smaller in magnitude and duration. Contingent on your specific situation including when you need to access your long-term investments, we suggest that everyone stay invested despite the noise. Market timing doesn’t work.

If You Are Not Invested, Get Invested (With Caution)

With markets reaching or nearing all-time highs in 2024, it is natural for some investors to wonder if it’s better to wait for a market pullback before committing capital. While this approach may seem logical, history shows it can often be counterproductive.

During bull markets, new highs are a frequent occurrence and waiting for a decline can result in missed opportunities. While the market returns of the past do not guarantee returns in the future, history shows that many times the eventual pullback only erases a portion of the growth that occurred since the prior low. Depending on your specific financial situation, if you have cash on the sidelines that is earmarked for long-term investing, consider putting at least a portion of that cash to work into the global markets on a regular schedule. While historical data would suggest putting it all to work in the global markets immediately, we must pay attention to the emotions of investing. Putting a large sum of money to work in the markets all at once, then watching the impact of a large pullback (should one occur soon after) is an extremely painful experience for most investors. Putting a portion of available cash to work on a regular schedule (dollar cost averaging) can help with the emotions that come with the inevitable market pullbacks that are impossible to predict.

Federal Reserve Policy and Inflation

The Federal Reserve navigated a complex economic environment in 2024, cutting interest rates by a total of 1% to support growth amid persistent challenges. By year-end, the federal funds rate settled at a target of 4.25% – 4.50%. But where do they go from here? The last cut in December was accompanied by comments that the path forward will be less certain than previously forecast. Their expectations are for two more rates cuts in 2025, but even their own current forecasts seem to conflict with that path.

Inflation continued to capture attention in 2024. Doesn’t it seem like prices on everything went up a lot more than 3.2% (headline CPI)? Remember that inflation comes from an increasing supply of money, not directly from government spending. The government collecting taxes or borrowing money from the private sector (people/organizations) to spend on their programs is only moving money from one place to another. In that circumstance, money supply hasn’t changed. However, the Federal Reserve creating new money to purchase bonds (Quantitative Easing or “QE”) does increase the money supply, the latest of which occurred from March 2020 through early 2022. This is what has led to our current battle with inflation. The money supply is slowing (Quantitative Tightening or “QT”), and we’re beginning to see signs of the corresponding slowing of inflation, but the change takes time to take effect.

Key Insights for Investors

- Stay the Course During Uncertainty: 2024 highlighted the importance of remaining invested during periods of actual and perceived volatility (storms). With market highs achieved during the year, many investors with long-term cash on the sidelines questioned whether to wait for a pullback. Attempting to time the market often leads to missed opportunities, while history suggests that a well-constructed portfolio can weather the short-term inevitable storms on its way to solid, long-term returns.

- Don’t Underestimate the Value of Diversification: Allocating across asset classes, geographies, and investment styles remains critical for optimizing returns and managing risk. The question isn’t only “What were my returns last year?”, but the equally important if not more important question is “How large of portfolio swings did I experience to get my returns last year?”. Diversification can help a portfolio receive the proper amount of return for the risk that was taken.

- Consider the Broader Picture: Market returns in your portfolio are only one of the important data points in your financial life. There are many other critical details to consider and plan for – insurance, tax, future or continued retirement, estate (planning for potential incapacity and for end of life), and charitable giving to name a few.

No one can predict what twists and turns we will experience in 2025. Like every year, there will be storms and triumph, certainly at the personal level if not also at the macro level. We are dedicated to helping you direct all of the details of your financial life towards long-term financial success. Our team is here to provide advice that is specific to your unique situation. Please feel free to reach out if you have questions or would like to discuss any part of your financial life in greater detail.

Warm regards,

Integrity Wealth Advisors