Hello, clients and friends, and happy summer to you. Our entire team at Integrity Wealth Advisors hopes that you are enjoying the first official month of the warm season. For those of us that live in Colorado, what a great time of year to be here. Our mission statement at Integrity is “to have an enduring impact on the community”. On June 18th, Larry Dozier and his team ran our 10th annual charitable golf tournament. We had a record number of golfers that raised a record dollar amount of $25,000 for the Children’s Literacy Center. It was a beautiful day of golf and camaraderie around a good cause. Activities like this fall perfectly in line with our mission and we hope you can join us next year for this memorable annual event.

The first half of 2021 turned out to be much better for the global economy and the investment markets than many had imagined. Is the upward trajectory legitimate or too good to be true? We are cautiously optimistic that it is legitimate and will continue. Time will tell. Let’s take a look at the data.

Where We Have Come From

| Asset Class | Index | 2nd Quarter 2021 | Year-to-Date 2021 | Last 12 Months | Three Years (Ann.) |

| US Stocks | Russell 3000 | 8.2% | 15.1% | 44.2% | 18.7% |

| Foreign Stocks – Developed World | MSCI EAFE | 5.4% | 9.2% | 32.9% | 8.8% |

| Foreign Stocks – Emerging Markets | MSCI EM | 5.1% | 7.6% | 41.4% | 11.7% |

| US High Quality Bonds | Bloomberg US Agg. Bond | 1.8% | -1.6% | -.3% | 5.3% |

| US High Yield Bonds | iBoxx Liquid High Yield | 2.0% | 2.6% | 13.0% | 6.4% |

Sources: ftserussell.com, msci.com, Eaton Vance Monthly Market Monitor, Y-Charts

The S&P 500 index (a good representation of large, publicly-traded US companies) ended the quarter at an all-time high. The international stock markets (Developed and Emerging), as represented by the MSCI World Net ex-US index, set a new high during the quarter on 6/16/21. Investment-grade bonds rebounded to have a positive second quarter after a challenging first quarter. The markets for the last three years, as evidenced by the three-year annualized returns listed above, have been strong. This time frame includes the negative fourth quarter of 2018 and the COVID-influenced first quarter of 2020. Both stock and bond markets have been resilient and continue to support our cautious optimism.

Looking Ahead

Have you been to an airport, restaurant, bar or campground lately? It is busy. There appears to be plenty of pent-up demand from consumers for such things. While that is a positive, it doesn’t represent all sectors. Let’s review a selection of financial metrics past and present that speak to the markets as a whole. Please remember that market returns from the past do not guarantee that we will experience the same in the present or future.

- As referenced in our prior newsletter, the average one-year bull market return after a 30% or more decline is 41% (S&P 500 Index). It has happened six times since WWII. Our bull market recovery since the markets bottomed from the COVID shutdown has been greater than that. That’s good, but what about the second year after a 30% or more decline? The average return in year two is 17%. (Data source is Horsesmouth)

- Over the past 67 years, the S&P 500 has gained more than 12.5% in the first half of a year 16 times. In 12 of those 16 years, the index experienced gains in the second half of the year as well. (Data source is Guidestone®)

- While the financial media take every opportunity to sensationalize any data point possible, we would agree with the reports that valuation multiples appear to be “stretched” right now. There are other measures we can consider to give a more complete picture. Valuation multiples are actually less correlated with stock market returns than earnings growth. From the 1960s and forward, for holding periods of greater than three years, the correlation between earnings growth and stock market returns has been very high, in the 80% – 90% range. So how well are earnings growing? Taking a look at 2021, earnings growth for US companies in the second quarter grew 65% year-over-year! While this is partly due to the low starting point from the COVID shutdown, earnings growth has also improved 10% when compared to the second quarter of 2019. Furthermore, while earnings growth data for US companies is strong, it is even stronger for international companies. (Data source is Neuberger Berman).

While the past can’t predict the future, and we are in unprecedented times, we would suggest that there is some support for continued gains in the stock markets over the rest of the year.

What about inflation?

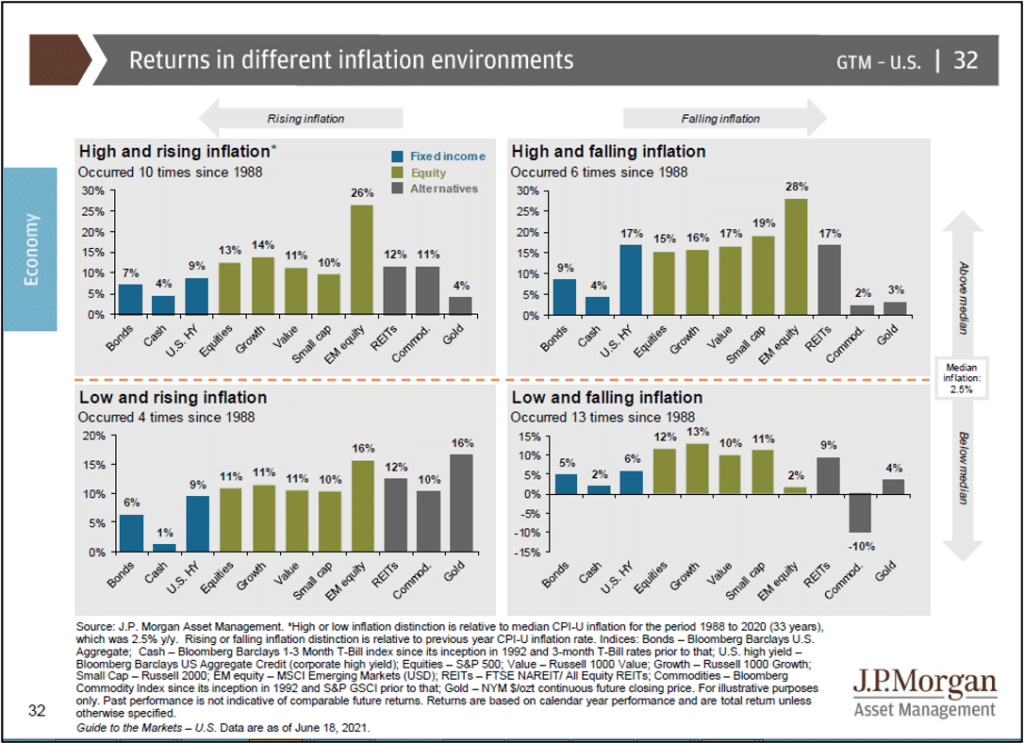

Multiple members of our Investment Committee spend time attending analyst phone calls and webinars to monitor the latest thoughts on all things financial. The recent consensus on inflation estimates for calendar year 2021 appears to be somewhere around 3%. That is certainly higher than we have experienced in a long time. The last year-over-year inflation increase of 3% or more was November 2011. There is plenty of debate about whether it is “transitory” or here to stay. JP Morgan provided an excellent chart (below) that provides average returns for various asset classes during times of rising and falling inflation. Please pay attention to the two quadrants on the left. According to their analysis, since 1988 there have been ten calendar years with a starting point of “high inflation” and an ending point with inflation that was even higher – defined as “High and rising inflation”. Additionally, since 1988 there have been four years with a starting point of “low inflation” and an ending point with inflation that was higher – defined as “Low and rising inflation”. As you can see from the left quadrants, over fourteen periods of rising inflation since 1988, all the major asset classes provided positive average returns. What we can take from this history is that rising inflation in the recent past has been far from disaster for investors.

If history and the financial data are wrong this time and we experience a stock pullback, please remember that market downturns provide fantastic opportunities for disciplined investors. Bonds (some of which tend to perform well when stocks are struggling) and cash should be part of a well-diversified portfolio for almost any investor. Using cash and appreciated bond proceeds to purchase stocks at discounted prices during pullbacks is an example of “rebalancing”. It is a time-tested strategy for investing success. This worked out beautifully during the COVID-challenged 2020 and we are confident it will continue to be beneficial in the years to come.

Thank you for taking the time to read through our thoughts on the topics above. Our entire team feels fortunate to be part of a great company and serve such excellent clients. For those of you who are not clients but are curious about who we are and what we do, please call us. We would welcome a chance to meet you.

Warm Regards

Jason Akridge, Vice President and Senior Advisor

Integrity Wealth Advisors