Hello, clients and friends of Integrity Wealth Advisors. We hope this finds you healthy and persevering in the midst of the continuing Covid-19 pandemic. We are all in this… and we will get through it together.

Integrity Wealth Advisors would like to acknowledge all the teachers and school administrators in our community. It is nothing short of remarkable what you are doing to keep our next generation engaged academically. Every week that our schools are open is another milestone! Thank you all!

The Latest Cliffhanger

President Trump and The First Lady tested positive for Covid-19 on the first day of the fourth quarter of 2020, injecting a new round of uncertainty into an already tumultuous 2020. We hope and pray for a speedy recovery for both. How this may play out with a presidential election less than a month away is unknown, as we’re in uncharted waters.

Flashback

Imagine yourself at the beginning of the 2020 calendar year. You have knowledge that within weeks a novel virus will emerge that will shut down much of the global economy. Businesses will close, sporting events will be canceled, your daily routine will be altered, travel plans will be derailed, and tens of millions of Americans will be thrown out of work.

There is no preventative vaccine, no cure, and the virus can be contracted like the common cold or the flu via airborne contact.

This will turn into a health and economic crisis that no one alive has ever experienced.

It sounds like a script created in a Hollywood studio. Yet, it’s the reality of 2020.

With the foreknowledge that a global pandemic and economic collapse was on the horizon, how might you have positioned your investment portfolio?

Many would have correctly anticipated a swift sell-off in stocks as the virus swept across the globe and the U.S economy went into hibernation. The safety of cash or long-term Treasury bonds would have been alluring.

But consistently picking the peaks and valleys in stocks, or even something close, is a fruitless endeavor. We know that intuitively.

When might the investors who had fled to safety decide to repurchase equities, returning to the proper asset allocation designed to achieve their financial goals?

Would the unending drumbeat of bearish sentiment have kept them out of the market and in the safety of cash or government bonds? For many, it’s difficult to pull the trigger when the news is bleak, and there’s no light at the end of a dark tunnel.

The swift sell-off in stocks is in the record books. It was violent but short-lived.

As the economy was on the precipice of its worst quarterly decline on record (St. Louis Federal Reserve GDP data, April – June quarter, quarterly records began 1947), the major market indexes touched bottom in late March and began a remarkable rally that few thought possible. The biggest monthly gains came in April. Many who exited the market in March didn’t have the resolve to get back in to participate in April’s gains. In all likelihood, for those investing with a long-term perspective, it was probably best to stay invested throughout the market volatility. Integrity Wealth Advisors remained disciplined, buying equities as the market fell so that our investment management clients’ could fully participate in the eventual rebound.

Third Quarter US Equities

The strong second quarter had everyone wondering if the equity markets were reading the same headlines as everyone else. But the third quarter came out of the gates strong supported by unprecedented liquidity supplied by the Fed, rock bottom interest rates, and an improvement in the overall economy. In fact, the headlines at the end of August pronounced that it was the best performance by the stock market in August since 1984!

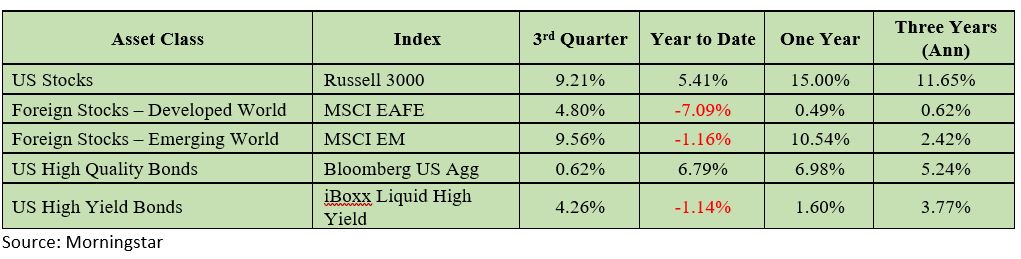

The Dow improved dramatically from the March lows but has yet to reach its pre-Covid highs and remains down -2.7% YTD. The S&P 500 Index set a new record on August 18 and proceeded to set six new closing highs by the end of August. In fact, the S&P 500 Index surged an impressive 60% from the March 23 bottom to the most recent high in early September (St. Louis Fed S&P 500 data).

Then stocks hit a roadblock in September. After closing at an all-time high on September 2, the Nasdaq Composite dropped more than 11%. Nevertheless, the technology-heavy Nasdaq has experienced a spectacular 24% advance through the first three quarters of 2020.

Table 1: Key Index Total Returns

Given the incredible run, a pullback was inevitable. The timing, magnitude and duration of a pullback is impossible to predict. Your success is based, at least in part, on time in the market, not timing the market.

There were several factors that played a role in the recent pullback in US Equities.

- Any uncertainty creates a good excuse to take profits after a big run-up in price.

- Daily Covid cases in the U.S. ticked higher last month, per Johns Hopkins data.

- While it won’t be cheap, Congress has yet to find common ground on a new fiscal stimulus bill. The economic bounce in Q3 was much stronger than most initially thought possible. But investors and many analysts believe more support is needed.

- Finally, the election is front and center. We may not have a winner on election night. Worse, a disputed election would add to investor angst.

In Other Asset Classes

U.S. Investment Grade Bonds have done their job well in 2020, bringing some stability to offset the volatility of the equity markets. The Bloomberg/Barclay’s Aggregate was up 6.8% year-to-date through the end of the third quarter, with US Corporate Bonds coming in at 6.6% YTD.

Foreign developed market equities (MSCI EAFE) are down -7% YTD. Emerging market equites (MSCI EM) had a strong third quarter, up nearly 10% QTD going into the last week of September but nevertheless ended September negative for the year, down -1.2% YTD.

Buoyed by low mortgage rates and pent-up demand, residential housing activity, a traditional leading economic indicator, has surged (U.S. Census data, National Assoc of Realtors, NAHB). However US Commercial Real Estate REITs, down -17% for the year, have been the biggest loser of all asset classes year to date.

In summary, there is a 41% spread between the best performing (Nasdaq) and worst performing (US REITs) asset classes year to date. As usual, asset allocation is a powerful determinant of overall investment performance. A “reversion to the mean” – or a return to historical average returns by asset class – may come at any time. Asset allocation requires the discipline to sell top performing asset classes to purchase downtrodden asset classes in preparation for the next reversion. That is why we at Integrity Wealth Advisors continually preach asset diversification and disciplined rebalancing of asset classes.

Back to the Future

With the foreknowledge that a continuing global pandemic and volatile election is on the horizon, how might you position your investment portfolio today?

Just as investor’s may have been tempted to retreat to cash had they known in January a pandemic was coming, investors may think now is a time to move to cash ahead of a contentious election.

But it is worth repeating: consistently picking the peaks and valleys in stocks, or even something close, is a fruitless endeavor. We would advise you to stay the course based on your risk tolerance and investment objective using a well-diversified portfolio routinely balanced with discipline rather than emotion. If you are investing with a long-term perspective, we recommend it will be best to just stay in the market throughout this election cycle.

As we head into the 2020 election amid acrimony on both sides, those of us at Integrity Wealth Advisors would like to remind you that our role is to be your financial advisor. We have worked hard to earn your trust. We are not political analysts. We are here to guide you as you journey toward your financial goals.

Therefore, let us carefully and cautiously review the current contest through a very narrow prism–through the eyes of a dispassionate investor focused on the economic fundamentals and how that might impact your portfolio.

Let’s consider these facts.

- Stocks have performed well under both parties historically.

- The conventional wisdom isn’t always right. Recall that stocks weren’t supposed to do well with a Trump win, as some investors believed a Hillary Clinton presidency would offer continuity… and markets don’t like uncertainty. But market returns under President Trump have been remarkable, making many forget the volatility that immediately followed the 2016 election.

- Compromise and gridlock may engulf a dominant party, as a one-sided win tends to expose party divisions. Remember how Republicans would quickly repeal Obamacare?

Some investors fret that a Biden win would lead to higher corporate taxes and heap more regulations on businesses. However, that is most likely only if there is a Democratic sweep of the presidency and both houses of Congress. It that case, might we see significantly more fiscal stimulus, which could support shares in the near term?

Nevertheless, if Biden is elected, his proposed tax hikes are significant. If passed those tax hikes may impact the earning per share of S&P 500 companies and, consequently, stock prices in the intermediate term… or not. Refer to market performance after the 2016 election.

As far as specific equity sectors, according to JP Morgan’s Meera Pandit, CFA: Policy, not politics, should have a more lasting impact on market returns. Under a second Trump administration, deregulation would likely continue, which has benefited financials and some of the more traditional energy companies. Both administrations would likely pursue large infrastructure packages, which could lift materials and industrials. Both parties have sought anti-trust measures for some of the leading technology companies, so any outcome is likely to put pressure on the technology sector.

Regardless of who is in the White House, should a divided government remain it would likely continue to curtail ambitious policy initiatives of either Trump or Biden.

Longer term, stocks march to the beat of the economy, Fed policy and corporate profits. A growing economy fueled by innovation and entrepreneurship has been the biggest driver of stocks over many decades. That’s not likely to change regardless of who is President.

Final Thoughts

We remain bullish on the long-term prospects for the U.S. economy, yet we are always monitoring short-term risks.

While markets don’t always get it right, they attempt to price in the future. Markets are made up of millions of investors that have a financial stake in their decisions. Current price action suggests the economy will continue to improve, though the pace of improvement is uncertain.

The economy may not be the same when the pandemic and election is behind us, but we are a resilient people, we will persevere, and we will adapt. We are all in this… and we will get through it together.