This time last year, the World Health Organization declared that the spread of Covid-19 constituted a worldwide pandemic. As we know all too well, stringent measures in the U.S. were being taken to slow the spread of Covid and “flatten the curve.” The lockdowns and shelter-in-place orders dealt a body blow to U.S. economic activity.

Consequently, investor reaction was swift, and the first bear market since 2009 descended upon investors. Volatility was intense. Seven of the 10 biggest one-day point drops (not percentage drops) in the Dow’s history, including the biggest – a nearly 3000-point drop in one day – happened between February 24 and March 18, 2020. (Standard & Poors)

The major market indexes bottomed on March 23, 2020. If we use the broader-based S&P 500 Index as our yardstick, the bear market lasted barely over a month. It was a swift decline, but it was the shortest bear market we’ve ever experienced.

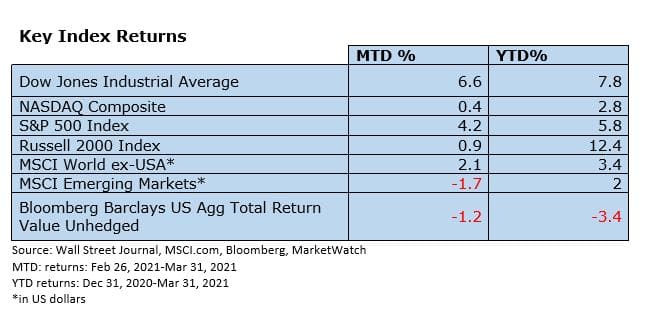

The ensuing rally has been historic. Since bottoming, the S&P 500 Index advanced an astounding 77.6% through March 31, 2021. As if to prove the rally isn’t just a one-year phenomenon, on April 1, 2021 the S&P 500 topped 4,000 for the first time ever.

Broader View

Reviewing the six longest bull markets since WWII, the S&P 500’s advance over this past year tops all other prior bull markets. In second place at 72.4% is the previously completed bull market that ended in February 2020, which began 11 years earlier in 2009 as noted above.

Let’s look at what’s happened in the second year of bull markets following bear markets in which the S&P 500 Index falls at least 30%. As always, past performance doesn’t guarantee future results. No one can accurately and consistently predict what will happen to stocks.

According to Horsesmouth, since World War II, there have been six other bear-market sell-offs of at least 30%. In each case, the market posted strong returns in the first year, with an average gain of 40.6%. Gains ran into year two, with an average increase of 16.9%; however, the average pullback during those six periods was -10.2%. So, let’s not discount the possibility of a bumpy ride this year.

Today, momentum favors bullish investors, but valuations seem stretched, at least over the shorter term. When markets are surging, there is a temptation to load up on risk. Yet, we’d counsel against being too aggressive.

Just as an investment plan we implement for our clients takes the emotional component out of the investing decision when stocks are falling, it also erects a barrier against the impulse to load up on riskier investments when shares are quickly rising.

Life changes, and when it does, adjustments may be appropriate. Ups and downs in stocks are rarely a reason to make emotion-based decisions in your portfolio.

American Rescue Plan

On March 11, 2021, President Biden signed the American Rescue Plan into law. This $1.9 trillion stimulus package aims to help around 158 million households continue to get back on their feet after a year-long struggle with the pandemic. This legislation contains many provisions assisting individuals, small businesses, state and local governments and schools.

The saying attributed to the late Senator Everett Dirksen seems almost quaint, “A billion here, a billion there, pretty soon, you’re talking real money.” Treasury bond yields have jumped as the government has embarked on this $1.9 trillion stimulus package and talk of a new $2.3 trillion infrastructure spending bill from Washington is gaining momentum.

Expectations that vaccines and new stimulus money will boost the economy, lifting growth and inflation, have reduced the appeal of fixed payments offered by bonds. Bond yields rise as bond prices fall. Falling bond prices recently pushed the yield on the benchmark 10-year Treasury above 1.7% for the first time since January 2020.

As bond yields go, so go mortgage rates. In March 2021, the average rate on a 30-year fixed-rate mortgage rose to above 3% for the first time since July 2020. Americans who purchased new homes or refinanced their current ones over the past year may have done so at just the right moment. (Mortgage Bankers Association)

Return of the Roaring 20’s

In March, President Biden stated that “we’re now on track to have enough vaccine supply for every adult in America by the end of May.” As of April 2021, about a third of Americans have now received at least one shot, according to the Centers for Disease Control and Prevention.

Some people are saying that the post-pandemic world is going to be like the Roaring ‘20s. After the Spanish Flu of 1918 everyone was ready to get out and be social. Similarly, as vaccinations in the country increase, we are starting to see people plan for summer activities and trying to get back to normal.

Americans currently have approximately $3.9 trillion in savings, up from $1.4 trillion before the pandemic. Pent-up demand and ample savings may be an explosive combination for growth in the coming year.

Jerome Powell, Chairman of the Federal Reserve, continues to hold the line on raising interest rates. In January 2021, he stated, “When the time comes to raise interest rates, we will certainly do that. And that time, by the way, is no time soon.” In an April 11 interview with 60 Minutes, Powell stated, “What we’re seeing now is really an economy… at an inflection point… where the economy’s about to start growing much more quickly and job creation coming in much more quickly.”

Bullish enthusiasm can sometimes spark unwanted speculation. Might the economy overheat and spark an unwanted rise in inflation? Might rising bond yields temper investor sentiment? At least for now, investors have chosen to focus on the rollout of the vaccines, reopening of the economy and the benefits these are providing.

Jamie Dimon, Chairman and CEO of JPMorgan, stated in his 2021 letter to shareholders that strong consumer savings, expanded vaccine distribution and the Biden administration’s proposed $2.3 trillion infrastructure plan could lead to an economic “Goldilocks moment” – fast, sustained growth alongside inflation and interest rates that drift slowly upward. (WSJ.com)

The Importance of Diversification

Much of 2020 was dominated by gains in the technology sector and other growth stocks. When one sector completely overshadows all others, as the tech-sector did in 2020, the other sectors begin to appear more appealing. As such, in Q4 2020 a rotation from growth stocks to cyclical stocks began to gain traction. Recent gains in value stocks are outpacing growth stocks by the widest margin in two decades in the latest sign that investors expect a robust and broad-based economic rebound. Value stocks include banks, energy companies and others whose fortunes are closely linked to economic growth.

The forward Price to Earnings (or “forward P/E”) ratio of the S&P 500 is 21.9 as of March 31, 2021. It has not been this high since the tech bubble in 2000 when it registered 24x. The forward P/E ratio is well above the 25-year average of 16.6x. (J.P. Morgan Asset Management)

As stated, part of the appeal of value shares is their lower price tags. At the end of February, the Russell 1000 Value Index traded at 21.89 times the past 12 months’ earnings, according to FTSE Russell. For the Russell 1000 growth Index, that figure was 37.22. Profits for the industrial, materials (primarily value stocks) and financial (primarily value stocks) sectors are expected to surge in 2021, rising 89%, 37% and 22%, respectively, from a year earlier, according to FactSet, while tech-sector (primarily growth stocks) earnings are forecast to grow 18% (WSJ.com).

Developed and Emerging Markets are another relatively undervalued opportunity when compared to 2020’s high-flyers. These markets are interest rate sensitive and provided strong returns in 2020. They have been impacted over the last few weeks by rising interest rates and the strengthening dollar. Nevertheless, if the dollar is eventually weakened with all of the recent stimulus spending, then developed and emerging market investments could do well again.

Where Do We Go From Here

Economists surveyed by The Wall Street Journal boosted their average forecast for 2021 economic growth to 6.4%, measured as the change in inflation-adjusted gross domestic product in the fourth quarter from a year earlier. With regards to unemployment, economists in the same WSJ survey now expect the largest December-to-December jobs gain on record, adjusting their expectations on average from 4.9 Million to 7.1 Million job gains just since the last survey in late 2020. (WSJ.com)

JPMorgan’s S&P 500 price target for 2021 (which hit 4,000 on April 1, 2021) is between 4,200 and 4,600. Goldman Sachs strategists believe the S&P 500 Index will reach 4,300 by the end of 2021. (J.P. Morgan Asset Management, Goldman Sachs Asset Management).

Goldman Sachs offers seven reasons why the S&P will continue to rise in 2021:

- Earnings are beating estimates and will remain strong.

- Federal Reserve is “on hold” until 2024.

- There is no alternative (TINA) as bond yields are so low.

- Stimulus monies could be invested in stocks.

- The $5 trillion currently in money markets will find its way into the stock market.

- A strong economy and a weak U.S. dollar attract foreign investors.

- Company buybacks will be on the rise in 2021.

Are there risks? Absolutely. As previously stated, inflation and bond yields must remain low for this “Goldilocks moment” to continue.

Conclusion

Regardless of where the markets go in 2021, your Integrity Wealth Advisors team is standing by ready to capture market returns within your selected risk exposure by using an asset allocation that is tailored to your personal risk appetite.