Preface to the Q1 Commentary

On April 2, President Trump announced new tariffs on nearly all major U.S. trading partners. These tariffs are “reciprocal” in that they correspond to tariffs each country imposes on U.S. goods and are on top of previously announced duties. The average tariff rate across countries is 25%, with rates for some as high as 49%. While the implementation of these tariffs was widely telegraphed by the White House, the level and scope are greater than many investors and economists expected. The immediate market reaction was very negative, first in the US and then beyond. On April 9, President Trump reversed course and declared a 90-day delay on tariffs for all countries that had not imposed retaliatory tariffs. Markets reacted very positively, but it is too early to know what will happen from here.

There are many arguments for and against tariffs, and the topic can be politically charged. Regardless of how we each feel about these measures, we can acknowledge that these tariffs – if ultimately imposed – do represent a significant change in the global economic system.

It’s important in times like these to remember that markets can be fragile in the short run but are resilient in the long run. Over the past century, markets have experienced significant global economic shifts including wars, recessions, bubbles, pandemics, political change, and technological revolutions.

In times of uncertainty, it can feel as if markets will never stabilize. Yet, history shows that markets can overcome even the most significant shocks, and often rebound when it’s least expected, as they did in late 2022 as the Federal Reserve raised interest rates, and as they dramatically did in late March 2020 during the pandemic. In fact, we just passed the five-year anniversary of the start of an amazing market correction which started in late March, 2020 while Covid was still raging. Anyone remember that?

Let’s take a deep breath, go for a walk on a sunny spring day, and seek some long-term perspective. Hopefully this commentary will also provide you with some near-term perspective. Now on to our regularly scheduled newsletter…

Q1 2025

The famous investor Peter Lynch once wrote that “far more money has been lost by investors trying to anticipate corrections, than lost in the corrections themselves.” The topic of stock market corrections, defined as declines of 10% or more from all-time highs, rose to the forefront in the first quarter as major market indices stumbled. The stock market has still made significant gains over the past few years. Amid ongoing market and economic uncertainty, it’s important for long-term investors to not lose sight of this fact.

Continued turbulence in financial markets is the result of tariffs on major trading partners and the possibility of reciprocal tariffs against many others. While there are concerns that a trade war could slow global economic growth, much of the market’s recent moves are simply due to uncertainty around what, when, and how these tariffs will be implemented. The possibility of higher prices for everyday goods and services has also raised concerns among consumers, feeding worries about inflation and slower spending.

In general, the stock market dislikes uncertainty since it makes it difficult to assess risk and determine asset prices. The wide range of possible outcomes only makes this more challenging, and is why markets experienced daily swings in the first quarter.

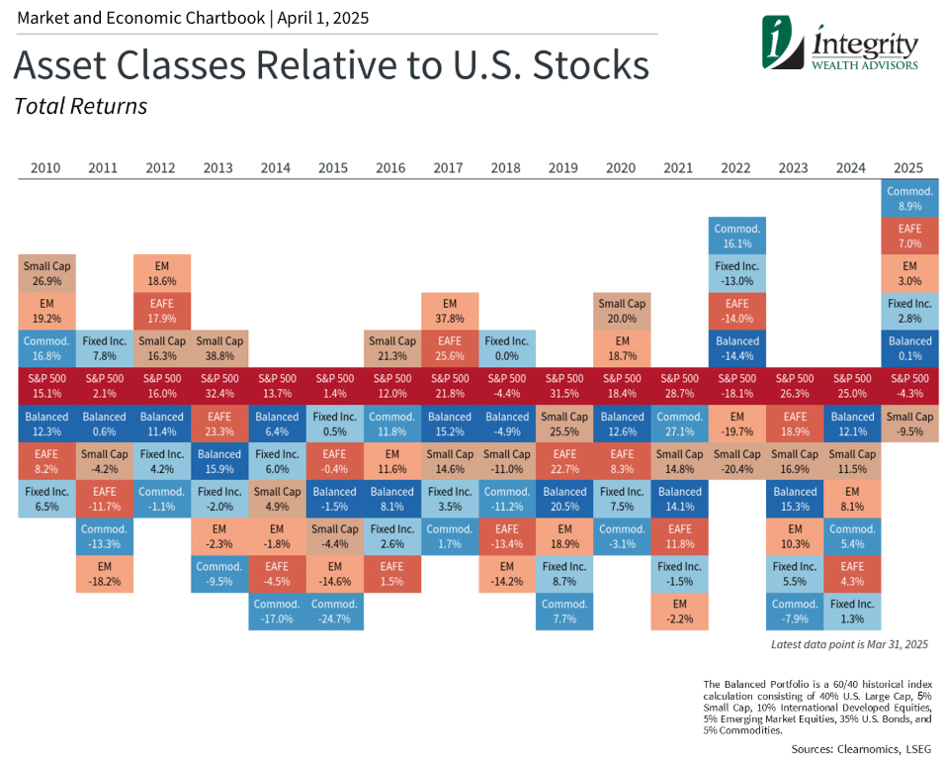

However, proper investing and financial planning is not about picking a single asset class or reacting to daily headlines. Instead, holding an appropriate portfolio that can withstand all phases of the market cycle is the best way to achieve financial goals. This approach has benefited from the many other asset classes that have supported balanced portfolios this year, including bonds, international stocks, and alternative assets such as commodities. This will be important to remember in the coming months as uncertainty continues.

Key Market and Economic Drivers

- The S&P 500 declined 4.6% in the first quarter of the year, the Nasdaq 10.4%, and the Dow Jones Industrial Average 1.3%.

- The Bloomberg U.S. Aggregate Bond index gained 2.8%. The 10-year Treasury yield ended the quarter at 4.2% after reaching as high as 4.8% in January.

- Developed market international stocks (MSCI EAFE) gained 6.1% and emerging market stocks (MSCI EM) increased 2.4% in the quarter.

- Gold rallied to a new record level of $3,122 per ounce.

- In the economy, headline inflation (Consumer Price Index) rose 2.8% year-over-year in March, while the Core measure, which excludes food and energy, rose 3.1%.

- The University of Michigan Consumer Sentiment index fell to 57, the lowest level since 2022.

- The Federal Reserve kept rates unchanged within a range of 4.25 to 4.5% in March, but slowed the pace at which assets will roll off its balance sheet.

Major stock market indices stumbled in Q1

The stock market experienced its first negative quarter since the third quarter of 2023. The chart above shows that the year-to-date return for the S&P 500 is in negative territory at this early point in the year. However, it also shows that this is quite normal for the stock market. Historically about two-thirds of years are positive while one-third are negative. Despite these down years, the stock market has grown steadily over history, across decades and market cycles.

As the second quarter begins, there is still a great deal of uncertainty. Beyond tariffs, where the market goes from here will likely depend on how corporate earnings and the economy perform, especially once there is greater clarity. Fortunately, earnings-per-share growth for the S&P 500 has remained strong, with current consensus expectations suggesting that earnings could grow as much as 12% in the coming year. While these Wall Street forecasts should always be taken with a grain of salt, they suggest that many stock market fundamentals are still strong.

For investors, bonds play an important role in these market conditions by offsetting the pullback in stocks. Bond prices tend to rise when interest rates fall since existing bonds with higher yields become more valuable. Thus, when the market struggles due to growth concerns, this often pushes down interest rates, which then support bonds and balanced portfolios.

In fact, many types of bonds have performed well this year including TIPS, mortgage-backed securities, Treasurys, and corporate bonds. This is a reversal of the past few years when high inflation and rising interest rates created the most challenging bond environment since the mid-1990s. This is also a reminder that a key principle of successful investing is holding a diversified portfolio that is aligned with long-term financial goals.

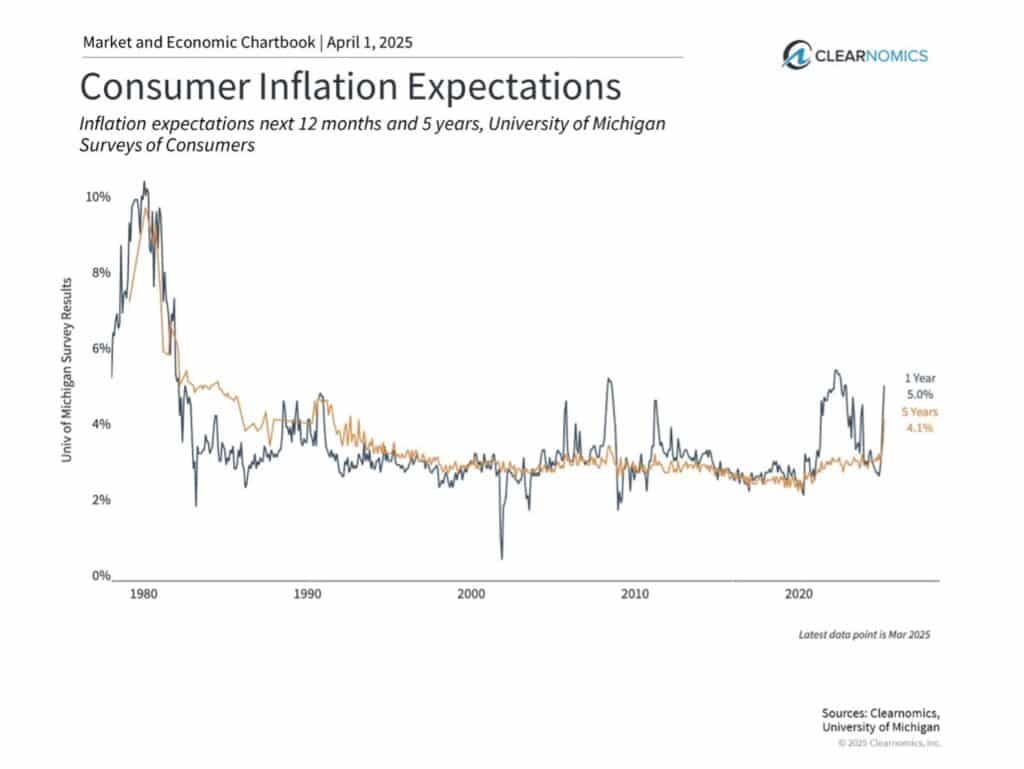

Tariffs have raised concerns among consumers

Trade policy weighed heavily on investors’ minds in the first quarter. According to the AAII Investor Sentiment Survey, individual investors became the most bearish they have been since 2022. Investors are still waiting for clarity on the size, scope and duration of tariffs.

The inflation outlook added to the uncertainty in the quarter. Key measures of inflation, including the Consumer Price Index and the Personal Consumption Expenditures Index, moderated during the first quarter of the year, but remained stubbornly above the Fed’s target of 2%. Some economists worry that tariffs will raise prices on imported goods, which will raise the prices of goods and services more broadly.

All of these factors weighed on consumer sentiment which continued to slide to historically low levels. In March, the University of Michigan Surveys of Consumers showed that consumers expect long-term inflation to be 4.1%, its highest level in three decades, in anticipation of higher prices due to tariffs. The one-year expectation of 5.0% is a sharp acceleration from last year when inflation continued to improve.

Given the inflation experience of the past few years, it’s not surprising that households are worried about higher prices. Counterintuitively, actual consumer spending remains relatively healthy. The robust job market, with unemployment still only 4.1%, has supported consumer income statements. Wages also continue to rise (even after accounting for inflation), leading to more financial stability even in the face of higher debt loads. While this isn’t true for all households across the country, these figures suggest that many are still in healthy financial shape.

Given limited visibility into trade policy outcomes, the Fed downgraded its outlook for the economy in 2025. Their March Summary of Economic Projections contains a forecast of just 1.7% GDP growth for the year, below 2% for the first time since 2022. They also expect more stubborn inflation, even while the job market remains strong.

Still, the Fed is not cutting rates despite weaker numbers since they view tariff effects as “transitory,” meaning they are one-off events that could fade over time. For example, tariffs on washing machines in 2018 highlight how, after an initial increase, prices stabilized. That period also underscores the fact that tariffs were used by the first Trump administration as a negotiating tactic to achieve longer-term trade deals.

Other asset classes have performed well this year

Bonds weren’t the only asset class to have a positive return in the first quarter. International markets also performed well with both developed market and emerging market stocks experiencing gains. International investing has been challenging the past several years due to both the outperformance of U.S. stocks as well as global economic and geopolitical challenges. The weakening U.S. dollar also helped to boost international stock returns, as the value of those assets in their local currencies increased.

This highlights the importance of investing across different asset classes, regions, and sectors, both in good and difficult markets. While a balanced portfolio is never the best performer, it creates a much smoother ride. This allows investors to focus not on short-term market moves, but on staying on track to achieve their long-term goals. When done well, it also has the benefit of allowing investors to sleep well at night.

The bottom line? Market uncertainty is never comfortable, but short-term swings are a normal part of investing. The first quarter serves as a reminder of the importance of holding a balanced portfolio to achieve long-term financial goals.

Bonus historical perspective – A Contrarian Consistency

“The VIX is the ticker for the Volatility Index on the Chicago Board Options Exchange. When it is going higher, fear in the market is rising; when it is going lower, fear is dropping; when it is stable, fear is level.

The VIX got to 52 (on Tuesday 4/8/25). From a historical perspective, one year after the VIX has closed at 45 or higher, the S&P 500 return has never been less than 18%, and it has averaged 39%. The return five years later (cumulative) has never been less than 100%, and it has averaged 139%.

Much of this is math – a very high VIX frequently (always?) coincides with a drop in the stock market, so the entry level in the market is, by definition, lower, if not outright low. But a lot of it speaks to a behavioral reality of investing – fear is often highest at the most opportune time, and fear is often lowest when there is reason for caution. We offer no prediction about where markets will be in a year or five years. However, when markets are dropping and the VIX is flying higher, history has had something to say.” (David Bahnsen, Dividend Café, 4/11/25)

Jeff Gott, CFP®

VP and Senior Financial Advisor

Integrity Wealth Advisors