Hello, friends, and welcome to 2022! We hope your holidays were healthy, happy and memorable. We were excited to host an Open House in December – our first client event in nearly two years – and we enjoyed the company of the 70 that visited with us. We are looking forward to our next in-person event (not yet scheduled) and hope to see you there.

Despite our desire that everyone enjoyed a prosperous and fulfilling year, we know that 2021 was a challenging time for many. We lost multiple clients due to various health challenges during the year and it was a reminder for all of us of the tenderness and brevity of life. Our condolences to everyone that lost someone.

From an economic and market standpoint, 2021 was another robust year and 2022 looks promising despite the potential challenges ahead (every year has its own challenges). Please read the data points below for 2021 and 2022 followed by the comparison of investment portfolios to the life and career of one of the most successful (and polarizing) football players of all time – Tom Brady.

2021 Economic and Market Data Points

Economic growth (GDP): Positive – The economy expanded strongly in 2021 with final real GDP growth estimated to be greater than 5%. This will be the best rate since the 1980s. While this number is impressive, it is partly reflective of the depths of the global economic shutdown due to COVID in the prior two years. We have not yet returned to the long-term average GDP growth rate of 2.0%, meaning that there is still room for additional economic expansion.

Employment: Positive – The US economy added a record 6.4 million jobs in 2021. The unemployment rate started the year at 6.7% and ended at 3.9%, which is close to the pre-pandemic low of 3.5%. Average hourly earnings for employees increased 4.7%. All data points confirm a positive environment for those that want to work.

Corporate profits: Positive – Corporate profits grew 68% during the year despite an increase in wage costs from the tighter labor market referenced above. Companies found efficiencies and were able to successfully pass on higher prices to their customers while seeing growth in demand for their products and services.

Inflation: Negative – Fuel expenses, used car values, home and rent costs, food prices – is there anything that feels like a bargain any more? Inflation skyrocketed in 2021 by 7%, a rate not seen for nearly 40 years. An increase in demand from higher wages and government payments, accompanied by a decrease in supply due to supply chain issues, both worked together to create the perfect storm.

Interest rates: Neutral (negative for some, positive for others) – Fed comments finally turned more “hawkish” this year as their inflation mandate was met and their labor mandate will be met very soon. Interest rates began to rise as a result. The 10-year Treasury note started the year at .93% and ended the year at 1.52%, a 64% increase.

Market returns: Positive (stocks) Negative (conservative bonds) – Despite the annual and predictable negative comments from certain members of the financial media to start the year, 2021 was another great year for developed world stock markets and diversified investors. It was a challenging year for emerging markets and fixed income. We would argue that strong equity returns were not based on speculative trading, but were based on the fundamentals referenced above. See the returns for the major asset classes below. Note the strong annualized returns for the three-year and ten-year periods which include the COVID pullback of 2020.

| Asset Class | Index | 4th Quarter 2021 | Full Year 2021 | Three Years (Ann.) | Ten Years (Ann.) |

| US Stocks | Russell 3000 | 9.3% | 25.7% | 25.8% | 16.3% |

| Foreign Stocks – Developed World | MSCI EAFE | 2.7% | 11.7% | 14.0% | 8.5% |

| Foreign Stocks – Emerging Markets | MSCI EM | -1.4% | -2.5% | 11.2% | 5.8% |

| US High Quality Bonds | Bloomberg US Agg. Bond | 0.0% | -1.5% | 4.8% | 2.9% |

| US High Yield Bonds | Bloomberg US Corp HY | 0.7% | 5.3% | 8.8% | 6.8% |

Data from Russell Indexes and Schwab Quarterly Chartbook

Summary: From an economic and market standpoint, it was a positive year overall for diversified investors, companies and the work force with the challenge of higher prices and limited supply.

2022 Economic and Market Data Points

Economic growth (GDP): Positive – GDP growth is projected to slow in the first quarter of 2022 (although still positive), then accelerate again for the remainder of the year. Support for this projection can be found from a continued increase in demand from consumers having more money to spend (increasing workforce with rising wages) and companies having to rebuild their low inventories.

Employment: Positive – If the jobs number continues to increase at the estimated 275k – 300k per month, the US should get to an unemployment rate of 3.5% by the middle of the year. As the latest variant of COVID appears to be less dangerous for most than previous variants, we should see more people re-enter the labor force.

Corporate profits: Positive – Corporate profits are estimated to grow another 10% in 2022. A reduction in supply costs as supply chain issues ease during the year, an increase in demand for products and services mentioned prior, and additional (but smaller) price increases should offset the pressure from rising wage costs.

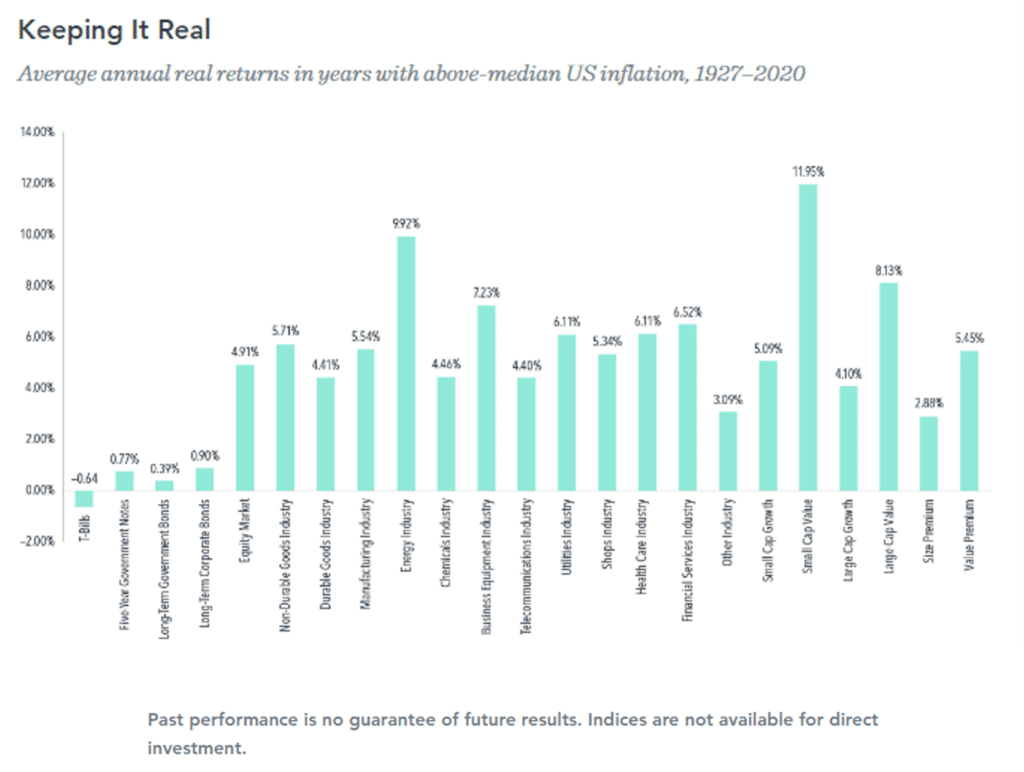

Inflation: Improving – Inflation is projected to slow to somewhere in the 3% – 4% range. During 2021, inflation for energy and food were 33.5% and 6.1%, respectively (through November 2021). It is highly unlikely that those levels will continue. Please keep in mind that many asset classes performed well during periods of heightened inflation in the past. The chart below from Dimensional Fund Advisors is another version of the data we provided in July last year. This chart provides average annual “real” returns (returns net of inflation) for a variety of bonds, stocks, and industries during periods of heightened inflation between 1927 and 2020. Inflation averaged 5.5% in high-inflation years. As you can see, there is only one negative return (1-month Treasury bills). The takeaway is not that we won’t experience negative returns if inflation stays elevated for a time as we suspect. The takeaway is that, on average, high inflation has not led to negative returns for many parts of the stock and bond markets in the past.

Interest rates: Neutral (positive for those that need income, negative for borrowers) – The Federal Reserve will raise the Fed Funds rate most likely three or four times in 2022. We would argue that this is overdue. As mentioned prior, the Fed’s two mandates have been met or will be met very soon. It will be helpful for bond yields to begin to return to more normal levels.

Market returns: Positive – According to data from the NYU Stern School of Business, there have been 26 years since 1950 that the S&P 500 Index exceeded 20%. In 77% of the years following, the index provided a positive return. Additionally, the average returns one, three, and five years after a new month-end market high are similar to the average returns over any one, three or five-year period. (Horsesmouth) Again, this is no guarantee that 2022 will provide positive market returns, but history and the current economic environment provide support for another positive year.

Summary: From an economic and market standpoint, there are ample signs that point to another positive year overall for diversified investors, companies and the growing work force with the challenge of higher costs for borrowers.

How Portfolios Relate to…Tom Brady?

We’re not sure what it is about this year’s college and NFL football seasons, but it seems like there has been a growing interest in the sport of late, at least in our local circles. One of the most polarizing and arguably best players to ever play the game (and who is still playing today) is Tom Brady. Tom spent most of his career as quarterback for the New England Patriots and is now in his second year with the Tampa Bay Buccaneers. It seems that most football fans either love him or hate him. Even within the walls of Integrity there are strongly opposing views. We see similarities between properly designed investment portfolios and his life and career.

Did You Know

Tom had a plan for his career if football didn’t work out. It’s humorous to think about football failure for him now, but when you’re the 7th-string quarterback at the University of Michigan, you need a backup plan. Tom interned at Merrill Lynch for two summers during college in preparation for life outside of a football career. For investors, what if markets don’t provide the investment returns that we hope they will? What if we need to retire earlier than we planned? Financial planning is an extremely important exercise for almost any investor, which includes a stress test of your financial situation for bad markets, an early demise, or other negative surprises. We don’t expect these things to happen just like Tom didn’t expect failure in football, but it is good to have a plan in place in case they do. Our team is constantly creating and updating plans for many clients to make sure they are prepared for whatever the future brings.

There are skeletons in the closet. Tom has a speckled past; Deflategate, Spygate, examples of poor sportsmanship after a loss. For many people those errors in judgment do not eclipse the overall body of work in his career. Welcome to the world of stock investing. There have been numerous times in the past where owning stocks or bonds has been painful, the most recent being the COVID pullback during early 2020. However, the overall body of work is impressive. Periods of heightened volatility should not overshadow the long-term returns that the markets have provided over the last 90+ years.

Tom lives an extremely disciplined lifestyle. His diet excludes sugar and dairy. 80% of his meals are vegetables. He ends each day at 8:30 pm. Discipline is one of the keys to his success. In much the same way, we believe that discipline leads to successful outcomes for proper investment portfolios:

- Diversifying holdings through low-cost ownership of stocks and bonds from around the world

- Tax efficiency through asset location of investments, tax-loss harvesting and Roth conversions

- Buying what is out of favor with investors and taking profits from what is in favor (rebalancing) when markets provide the opportunity to do so

He trains differently than most athletes. Tom avoids traditional weight training for football players and instead focuses on pliability and flexibility. Similarly, we are unlike many of our competitors who are tactical portfolio managers (e.g. moving into and out of the markets based on guessing the future, stock-picking). We are strategic in our approach. First and foremost, get the allocation decision right. Rebalance when the markets provide the opportunity (e.g. March 2020), stay fully invested and trim winners when appropriate. Keep costs low.

He has never had a losing season as a starting quarterback. In a testament to his talent, the talent of those around him, his preparation and his attention to detail, the worst record for a team that he has quarterbacked is 9 – 7. That is an impressive history. According to an analysis by Vanguard, a 60/40 “Balanced” portfolio has provided positive returns 77% of the time over the last 95 years, with an average annual return of 9.1%. No, unfortunately diversified portfolios can’t provide a winning record every year, but they have a long history of doing very good things for disciplined investors.

Tom has out-punted his coverage. He married above his station in life. You would think that career earnings of almost $300 Million would make him the higher-earning spouse. But his wife, supermodel Gisele Bundchen, has earned more in her career and is projected to have a much greater earning capacity going forward. We can’t think of an application of this to an investment portfolio but couldn’t pass up the chance to make the point.

Final Comparisons

44-year old quarterbacks shouldn’t be performing at their peak during the tail end of an incredible career. Love him or hate him, Tom Brady is doing exactly that. There are no guarantees that he can continue at this level but he’s doing all he can to continue. Similarly, many people can’t accept the fact that the global markets could continue on their upward trajectory after three years of impressive performance. There are no guarantees that they will but there are data points that suggest they can. However, unlike the career of a football player that inevitably comes to an end, when it comes to the investment markets, sell-offs are followed by rebounds and disciplined investors can take advantage of those opportunities. We have done that for our clients in the past and will continue to do that in the future. We are ready for whatever the markets bring. We’re in this together.

To our clients, thank you for allowing us to make a living doing something that brings us much fulfillment. To those of you that haven’t worked with us yet, we are here when you are ready.

Stay safe and healthy in this New Year.

Jason Akridge, Vice President and Senior Wealth Advisor

Integrity Wealth Advisors

The information in this communication was pulled from a variety of sources, to include Vanguard, Schwab, Dimensional Fund Advisors and others referenced within the commentary.