Hello, clients and friends, and welcome to the New Year. Our entire team at Integrity Wealth Advisors hopes that your December holidays were a time of thankfulness and refreshment. We know that 2020 brought the loss of loved ones and livelihoods to many, and we offer our deepest sympathies to all. May renewed health and a sense of optimism be in everyone’s future as we move into 2021.

Last year was a year like no other. What other year in history can claim a global health crisis, unprecedented shutdowns, historic stimulus efforts and one of the most contentious US elections in history? Just for good measure, let’s also throw in the first bear market for US Large Cap stocks (both the S&P 500 and the Dow) in over a decade and a corresponding rebound to new highs before closing the books on the year. 2020 will be discussed and analyzed for many years to come. What have we learned?

What Have We Learned?

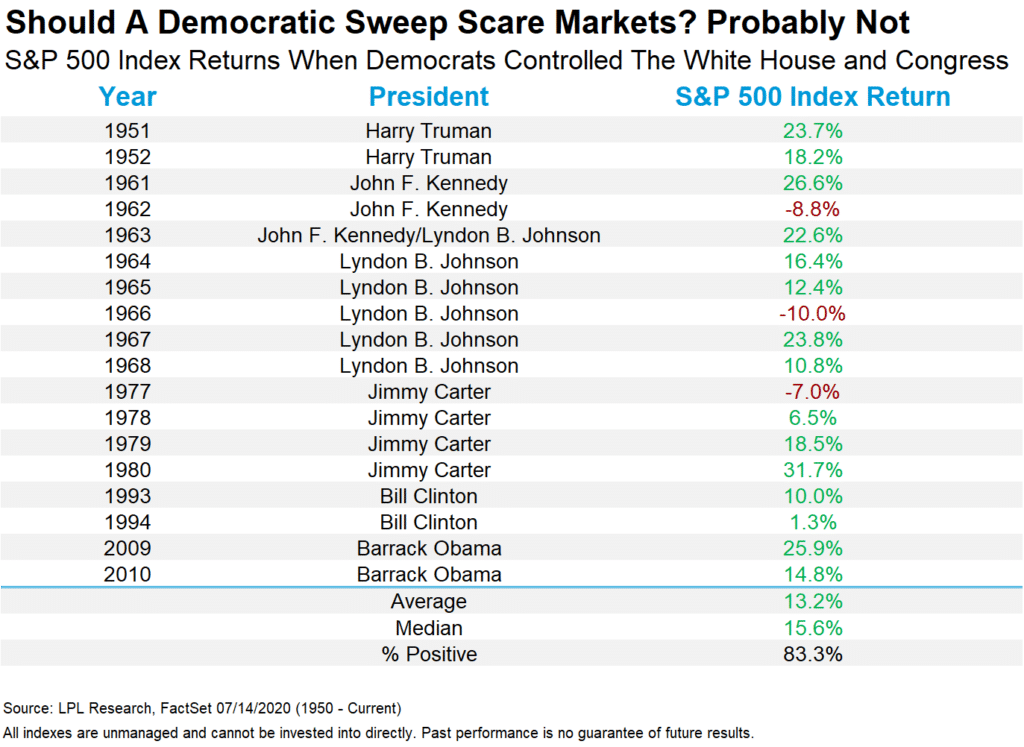

Political divisiveness is growing but Congressional majorities are not – What a painful election season to watch unfold. The attacks, the rhetoric and the demonstrations were all unsettling. While the Democrats now control the White House and both houses of Congress, their majority in the Senate is barely that and their advantage in the House of Representatives was considerably reduced (from 235 vs 199 to 221 vs 211 with vacancies). Given the near parity, we are hopeful that the two parties can work together to do what is best for our country. Nonetheless, should we be concerned about the impact of a Democratic sweep on the stock market? The chart below provides market returns for the S&P 500 Index when this has occurred in the past.

The results reveal that in most years of a Democratic sweep, the markets did quite well. If we provided the data for the years when the Republicans were in control of all or when there was split control, you would see similar results. The fact is that most analyses like this reveal that there is virtually no correlation between market returns and the party in power. Market returns tend to be driven more by things like economic cycles and investor sentiment.

While Congressional majorities are not growing, government spending is growing rapidly – The stimulus measures enacted by Congress have been helpful to many individuals, businesses and the economy, but they represent a massive bill that will need to be paid in the future. This has to be dealt with at some point. Unless we think the government will move to cut spending post-COVID (show of hands anyone?), tax revenues will have to be increased to pay the bill. Tax planning will be even more critical for you in the future. More on that below.

The American economy and global stock markets are resilient – If you think back to the dramatic pullback in March of last year, would you have guessed that our economy would rebound so strongly in the following nine months, or that the global stock markets would recover so well with US markets surpassing prior highs? The table below provides total returns (price change plus dividend and interest income) for the major asset classes around the globe as of December 31, 2020. We have provided returns for the first quarter of 2020, the full year 2020 and three years (annualized). We have also included calendar year 2019 as a comparison.

After a terrible first quarter, all of these asset classes had strong returns over the final three quarters and ended the year with healthy results. It took resilience to stay invested during that first quarter, and for those that did it turned out to be a surprisingly strong year for both stock and bond investors despite the mayhem. Is it realistic to believe that market returns could be positive again in 2021?

Looking Ahead

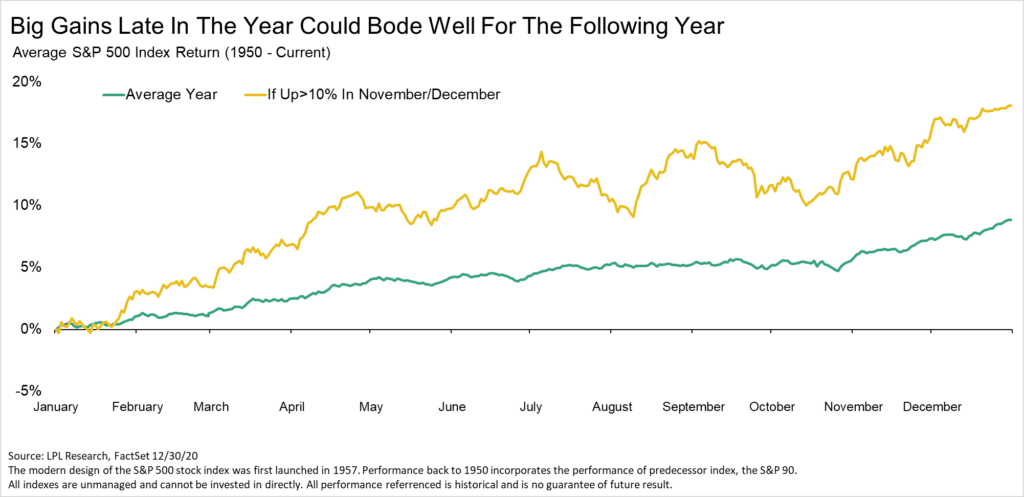

Market Returns for 2021 – No one can predict the future and we will not try to do that here. Some analysts are calling for positive returns in 2021. What data is there to support their claims? One point can be made by reviewing history for trends. The S&P 500 Index provided total returns (price change plus dividend income) of 10.9% in November and 3.8% in December last year. The chart below provides some interesting data.

The green line represents average returns for the index for each month of the year from 1950 through the end of 2020. The gold line represents the same data, but only for those years when returns for the prior November and December were greater than 10% (which is what occurred in 2020). The results of the analysis look encouraging. As you hear us say time and again, past results are no guarantee of the future but this historical trend does provide some support for analyst predictions. We are hopeful that they are right.

Do Not Fear Market Pullbacks – If history is not a guide this time and the bullish analysts are wrong, should we be afraid? Market downturns provide fantastic opportunities for disciplined investors. For many, there is never a better buying opportunity than in the midst of one. For our clients with diversified, public market portfolios, we rebalanced their accounts in the middle of March by trimming their bonds and buying stocks. Those stock investments have rebounded 30% to 65% or more in the short time since then. Rebounds to prior highs do not always occur quickly but this time they did, and we are thankful for what happened between April and December.

On a side note, for those of you with friends or family that decided to pull out of the markets last year, when did they decide to get back into the markets? Have they re-entered yet? One reason that we encourage investors to stay fully invested is because of the non-predictive nature of bad markets. For those that moved to the sidelines during late February or March until things felt “safe” again, they likely missed the best month of the rebound. The best performing month for the entire year was April when the S&P 500 Index returned 12.8%. For those invested for the entire year, the index returned 18.40%. If an investor missed the month of April, their returns for the year in that index were only 4.95%, a dramatic difference.

For some of our clients with “taxable” investment accounts (e.g. joint account, trust account), we captured tax losses during March. Those losses can be used to offset capital gains and earned income both now and in the future. While experiencing a market pullback can be painful, if managed properly it can actually be accretive to long-term portfolios.

Preparation For Potential Changes – From a financial perspective, what changes might be coming this year? We expect the new administration to work to raise income tax rates, possibly change long-term capital gains tax rates to the much higher personal income tax rates, lower the estate tax exemption and keep interest rates “lower for longer”. This does not spell doom for your financial situation or your investments. For our clients for whom we provide financial planning services, we can help you prepare for each of these by discussing the various strategies for limiting your tax bill (both current and future), and by stress-testing your plan for higher tax rates and lower bond yields. For our investment management clients (where appropriate), we will continue our work of tax-minimization by implementing such things as asset location strategies, capturing tax losses, managing the balance between bond duration and interest income, processing qualified charitable gifts, and using tax-efficient investments.

Taxes aren’t the only thing that will most likely be different going forward. To quote the Greek philosopher Heraclitus, “The only constant in life is change”. We know that change in life is inevitable and all of us have experienced that in multiple ways over the last year. None of us know yet what life will look like post-COVID. While we wait for a return to some version of normalcy, we know that things will be different and we will have to adjust. All of us can grow from this. We can adapt. We believe the best years are still ahead of us.

Our Integrity Wealth Advisors team feels blessed to serve our clients, many of whom are also friends. Thank you for giving us the opportunity to work with you. For those of you considering a relationship with us, we would love to talk with you about who we are, what we do and why we do it. Contact us today!

Sincerely,

Jason Akridge, CFP®, CWS®

Vice President and Senior Financial Advisor